I asked ChatGPT and Auryth the same Belgian tax questions — here's what happened

Three tax questions, two AI tools, one clear lesson: for professional research, verifiability beats confidence.

By Auryth Team

You’ve done it. Your colleague has done it. At some point in the last two years, every tax professional in Belgium has typed a fiscal question into ChatGPT.

The answer probably sounded reasonable. Maybe even impressive. But here’s the question nobody asks afterward: how would you verify it?

We ran a simple experiment. Three Belgian tax questions of increasing complexity — the kind a fiscal professional handles weekly. We asked ChatGPT (GPT-4o) and Auryth TX, our purpose-built Belgian tax research platform. Same questions, same day, no prompt engineering tricks.

The results reveal something more interesting than “right vs. wrong.”

Question 1: “What is the current Belgian corporate tax rate?”

ChatGPT answered correctly: 25%, with the reduced rate of 20% for SMEs on the first €100,000 of taxable profit. Clear. Accurate.

Auryth gave the same numbers — but cited Art. 215 WIB 92 directly, linked to the specific provision, and flagged the conditions of Art. 215, paragraph 3: the remuneration requirement and the participation threshold.

Both tools nailed the number. But only one showed why it was right and what conditions apply. When your client asks “do we qualify for the reduced rate?” — the confident number is a starting point. The sourced answer is a foundation for advice.

The gap between a correct number and a verifiable answer is where professional liability lives.

Question 2: “What is the TOB rate on an accumulating ETF?”

This is where it gets interesting.

ChatGPT answered: 1.32%. Stated confidently. No caveats.

That answer is incomplete. TOB rates for ETFs are 0.12%, 0.35%, or 1.32% depending on the fund’s characteristics. An accumulating ETF registered in Belgium pays 1.32%, but the same accumulating ETF registered elsewhere in the EEA pays just 0.12% — an elevenfold difference. Whether a fund counts as “registered in Belgium” depends on whether any of its compartments are registered with the FSMA. Distributing ETFs pay 0.12%. Non-EEA instruments: 0.35%. A professional advising on an ETF purchase needs to know the specific fund’s registration and distribution status — not just a single rate.

Auryth identified all three applicable TOB rates, explained the classification criteria — registration location, accumulating vs. distributing, EEA status — and flagged which rate applied to the specific fund in the question.

This is classification blindness — a failure mode of general-purpose AI. ChatGPT picks the most common answer and presents it as the only one. Belgian tax law is full of classification dependencies: rates that shift based on product structure, registration, domicile, and holding period. An AI that collapses these distinctions into a single confident number isn’t just incomplete — it’s dangerous for professional advice.

; Magesh et al. (2025), Stanford HAI")

Question 3: “What are all the tax implications of a TAK 23 insurance product for a Belgian resident?”

Now we’re in professional territory.

ChatGPT identified income tax (mentioning Art. 19bis WIB for the Reynders tax on capital gains) and insurance premium tax. Two domains. Presented with the same unwavering confidence as Question 1.

It missed three:

- Gift and inheritance tax — critical for estate planning, governed by the Vlaamse Codex Fiscaliteit (VCF) in Flanders, Code des droits de succession in Wallonia and Brussels

- TOB exemption — switching funds within a TAK 23 wrapper incurs no stock exchange tax, unlike direct ETF transactions. ChatGPT didn’t flag this key structural advantage

- Securities account tax (effectentaks) — the annual 0.15% tax on securities accounts above €1 million, which can apply to TAK 23 products through the look-through principle

A TAK 23 product touches at least five tax domains. ChatGPT covered two. The three it missed are exactly where clients lose money and advisors face liability claims.

Auryth structured its response as a cross-domain analysis: a domain radar identifying all five areas, per-domain conclusions with authority-ranked sources, confidence scores (high for income tax, moderate for regional variations given evolving case law), and a “gaps identified” section noting what wasn’t found.

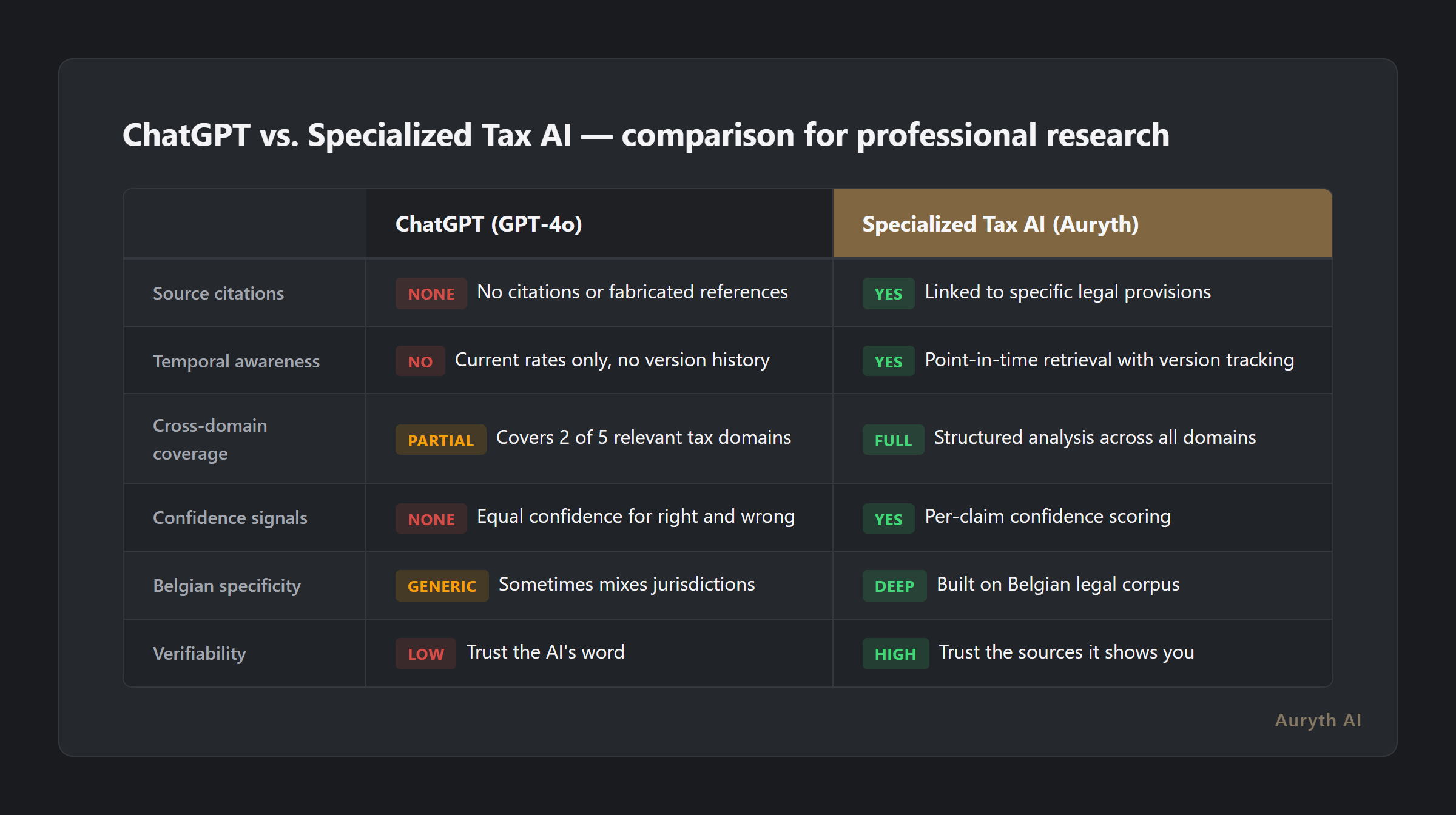

| Dimension | ChatGPT | Specialized Tax AI |

|---|---|---|

| Source citations | None or fabricated | Linked to specific legal provisions |

| Temporal awareness | Current rates only | Point-in-time retrieval with version history |

| Cross-domain coverage | Partial (2 of 5 domains) | Structured multi-domain analysis |

| Confidence signals | Equal confidence for everything | Per-claim confidence scoring |

| Belgian specificity | Generic, sometimes mixes jurisdictions | Built on Belgian legal corpus |

| Verifiability | Trust the AI | Trust the sources it shows you |

The verification gap

The pattern across all three questions isn’t about accuracy. It’s about verifiability.

ChatGPT may get the simple answer right. But it never tells you:

- Where the answer comes from (no source citation)

- When the answer applies (no temporal context)

- What’s missing from the answer (no coverage assessment)

- How confident you should be (no uncertainty signal)

We call this the Verification Gap: the distance between an AI’s stated confidence and your ability to independently check its claims. The wider the gap, the greater the professional risk.

For a quick Google search, the Verification Gap doesn’t matter. For professional tax advice — where wrong answers carry financial and legal consequences — it’s everything.

A tool that’s 90% accurate and honest about it is safer than one that’s 95% accurate and never tells you when it’s wrong.

But let’s be honest — specialized AI isn’t perfect either

Stanford researchers found that even purpose-built legal AI tools like Westlaw AI and LexisNexis+ AI hallucinate 17–33% of the time. RAG — retrieval-augmented generation, the architecture behind most specialized legal AI — reduces hallucinations dramatically compared to the 58–88% rate observed in general-purpose LLMs. But it doesn’t eliminate them.

The difference isn’t perfection. It’s transparency. When a specialized tool is uncertain, it tells you. When it cites a source, you can check it. When it misses something, a well-designed system flags the gap rather than presenting a partial answer as complete.

Belgian tax law contains genuine ambiguities: rulings that contradict circulars, regional variations that diverge, provisions with multiple valid interpretations. No AI should pretend otherwise.

The three-layer test

Before relying on any AI-generated tax answer — ours included — apply three checks:

| Layer | Question | What failure looks like |

|---|---|---|

| Source | Can you trace the answer to a specific legal provision? | ”The rate is 25%” with no article reference |

| Precision | Does the answer account for all relevant conditions? | One rate given when three apply based on fund characteristics |

| Completeness | Has the tool checked all relevant tax domains? | Two domains covered when five apply |

If any layer fails, you’re not doing research — you’re gambling with your client’s money and your professional reputation.

Related articles

- What Is RAG — And Why It Matters for Tax Professionals

- AI Hallucinations: Why ChatGPT Fabricates Sources

- What Is Confidence Scoring — And Why Is It More Honest Than a Confident Answer?

How Auryth TX applies this

Auryth TX is built specifically for Belgian tax professionals who need verifiable answers, not confident guesses. Every response includes:

- Authority-ranked source citations linked to specific provisions from WIB 92, VCF, WBTW, and the broader Belgian legal corpus — ranked by legal hierarchy

- Temporal versioning — ask about any date and get the version of the law that applied then, not just today’s version

- Cross-domain detection — automatic identification of all tax domains a question touches, with structured per-domain analysis

- Confidence scoring — explicit indication of how well-supported each claim is, including what the system searched for but did not find

The goal isn’t to replace your judgment. It’s to give you the complete picture — with sources — so your judgment has the best possible foundation.

Try it yourself — ask Auryth and ChatGPT the same question and compare.

Sources: 1. Dahl, M. et al. (2024). “Large Legal Fictions: Profiling Legal Hallucinations in Large Language Models.” Journal of Legal Analysis, 16(1), 64–93. 2. Magesh, V. et al. (2025). “Hallucination-Free? Assessing the Reliability of Leading AI Legal Research Tools.” Journal of Empirical Legal Studies. 3. Lewis, P. et al. (2020). “Retrieval-Augmented Generation for Knowledge-Intensive NLP Tasks.” NeurIPS. 4. EY Nederland (2023). “Is ChatGPT uw nieuwe belastingadviseur?”